Derryn Faure, Institutional Trade Finance, Investec and Ahanna Anaba, Head of Sales – Digital Solutions & Partnerships, Finverity, explain the reasons behind this pioneering collaboration

The media’s overwhelming focus on climate change, as important as it is, risks undermining attention to other pressing world needs. It’s therefore timely to note that only four of the 17 UN SDGs (sustainable development goals) directly address climate change. When formulating ESG frameworks, the focus of western economies has been on the environment but should that also be Africa’s primary focus. Remember that Africa only contributes 2% of global carbon emissions. Or to put it differently, should Africa be paying more attention to caring for the environment over and above ending poverty and hunger, which is an immediate need not necessarily relevant for western economies

African trade finance represents a unique opportunity for investors seeking an asset class that comprehensively supports the SDGs. International trade finance plays a crucial role in stimulating job creation and is estimated to contribute up to 30% of GDP growth in Africa, a continent in which SMEs are a key driver of growth and employ as much as 85% of the population in some African countries. Nevertheless, and despite the supporting evidence, we are far from fully appreciating the huge sustainable impact that African trade finance brings about in the SME sector.

In recent years, a significant amount of ESG-linked liquidity has been earmarked globally for SME lending. The challenges in accessing this liquidity are two-fold: the impractical requirements from development financial institutions (DFIs) to verify the trade finance nature of the lending; and the newer ESG compliance requirements (and by this we mean the requirement to prove the “E” part of ESG, seemingly to the exclusion of the “S” and the “G”).

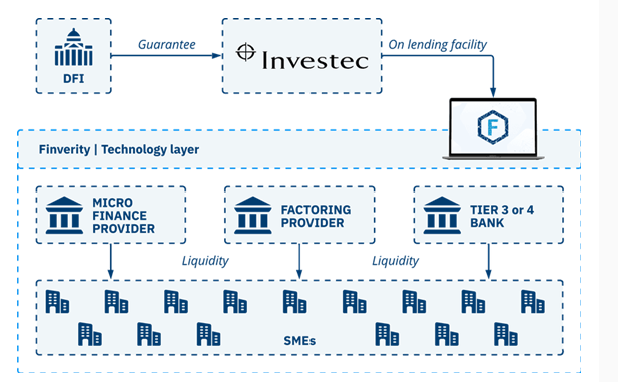

The evident solution to proving that the relevant financing is for trade and is in line with ESG standards is to go digital. The beauty of good digitalisation is that a much wider range of ESG metrics can be monitored and measured at the borrower level, directly at source, and in a more granular manner, especially for the S and the G. Good examples could include capturing data on the percentage of profits being reinvested locally by a company, educational targets, improvements in living and working conditions, and many others, depending on the borrower’s context. However, in Africa at present digital sophistication and data granularity lags far behind western markets in this area of trade finance. The collaboration between Finverity’s technology and Investec’s onward lending provides a solution to these two challenges.

For African SMEs to realise their full SDG potential, a truly data-led and comprehensive approach that appropriately measures and values the S and the G more equitably, and not only the E, is therefore required. To achieve this, DFIs and multilateral organisations must explore and deploy processes that fully value the contributions of each of E, S and G in ESG.

The appropriate ESG scoring metrics need to take into account the specific geographies (Africa vs Europe) and the product types (trade finance vs debt). Such factors have a huge impact in determining the appropriate sustainable / ESG taxonomies and principles deployed. The use of more appropriate and relevant metrics would therefore lead to more opportunities for African SMEs to access the millions of dollars available from DFIs and multilaterals to finance SME trade.

In a recent study on supply chain finance (SCF), the World Trade Organisation (WTO) highlighted the power of digital SCF solutions in bridging SMEs’ funding gap. While SCF facilities are common among tier 1 and tier 2 banks, such programmes are usually targeted at the multinational and blue chip companies in Africa – often leaving out the SMEs who would be the ones standing most to benefit from such facilities. As a result, the bulk of SME financing across Africa is carried out by lower tier banks and non-banking financial Institutions (NBFIs). However, the bulk of SMEs are severely constrained for reasons we explore below.

The fundamental obstacle to SMEs’ growth lies in the difficulties they face in obtaining trade finance and foreign exchange from financial institutions.

It is only through digitalisation of trade and fintech disruption that access to funding for African SMEs can improve. This will provide real time, digital processes and granular criteria against which funding can be drawn down. Achieving this will be a game changer, enabling DFIs and impact funds to support the lower tier banks and NBFIs who actually service these SMEs. By effectively tracing the flow of capital in real time rather than relying on contractual obligations that are back-dated, high-level digital reporting will open the doors to larger amounts of trade finance becoming available to African SMEs.

Innovative and next-generation technology will enable financiers to address the financing needs of a greater number of SMEs that previously struggled with accessing finance. It opens the door to:

Mass onboarding of SMEs in a cost-effective manner, e.g.

- Corporates can report data seamlessly through accounting systems, user-friendly onboarding and data dump screens

- African-orientated technology can boost adoption and provide dependable storage of key ESG metrics

Financiers can easily share data in bulk for reporting purposes, e.g.

- Monitoring of location and type of goods involved in the trade as well as age and nationality of ultimate beneficial ownership and management

- Collection and monitoring of company financials and business metrics to assess the impact of funding over time

Asset managers and DFIs can compare deployment channels and have a real-time view of fund manager performance and ESG impact across mandates, e.g.

- Leverage transaction data and generate forward-looking data to better assess risks and improve credit models.

The benefits of innovative and next-generation technology are immeasurable. As with all complex issues, however, the solution has to start with a simple framework. The first step is to provide an easy, digital method to collect, store and share data. This should be coupled with the incentives and technical support budgets for data to be shared and maintained by smaller financial institutions.

Aside from properly defining the ESG scoring metrics, reward systems should be incorporated to encourage both SMEs and their financiers to accurately report sustainability data. This will encourage transactions that are more closely aligned to sustainability goals.

Lower-tier banks and NBFIs will need support in building out their capacity to execute and scale these SME financing facilities. Equally as important, capital earmarked for SME funding needs to be made available through them. By beginning to standardise SME lending initiatives and processes, technology can pave the way for a truly scalable trade finance offering that adheres to the appropriate ESG objectives across Africa.

The prevailing market myth has been that developing lower-tier banks and NBFIs that can build out their capacity to execute SME financing facilities at scale would be a near impossible task. The results from Finverity’s Emerging Leaders Programme (ELP) shatter this assumption and speak for themselves. In only five days and using fully digital channels, in July 2022 Finverity sourced 70 applications to its ELP from over 25 countries in Africa. These smaller banks and NBFIs serve the SME sector directly and have funded a cumulative US$500m in 2022 based on data reported in applications to the programme.

The ELP is now equipping these banks and NBFIs with the technology, knowledge and implementation of the robust processes required to operate lending facilities safely and to the required ESG standards. We are therefore strongly encouraged by having found a way to boost the social impact of the SDGs thanks to a practical and feasible model that can funnel capital into SMEs in the real economy. Just as encouraging is that this can be achieved in the short term.

To tackle sustainability and truly grow the African SMEs of tomorrow, we must begin to break the barriers to SME trade finance and nurture the SMEs of today. The vast majority of suppliers in the African supply chains are SMEs, and the trade finance gap will simply not be filled through traditional banking methods. Over the years, potential solutions to this problem have been the subject of much debate.

Through an innovative collaboration, Investec and Finverity have decided to get the ball rolling by piloting SME-focused onward lending programmes using digital solutions that capture key sustainability metrics. This collaboration builds on the earlier success of Finverity’s ELP.

This collaboration will identify and provide key SME lenders across Africa with onward lending facilities, further digitalise their trade finance operations and improve crucial data-gathering processes. We believe that this will not only stimulate economic growth, but also increase intra-African trade and young but vital value chains to mature. More notably, this is the first step towards a verifiable avenue for tracking key ESG metrics, and truly addressing the ‘S’ and the ‘G’.

It is clear that the future of delivering inclusive, sustainable and scalable funding programmes for Africa’s SMEs will be driven by digital transformation. It will only truly scale, however, once liquidity providers, guarantee providers, SME-focused lenders and technology providers all work together. It is time for the development finance institutions, impact-focused funds and other trade finance players in the market to play their part.

To read more news and exclusive features see our latest issue here

Never miss a story… Follow us on:

![]() International Trade Magazine

International Trade Magazine

![]() @itm_magazine

@itm_magazine

![]() @intrademagazine

@intrademagazine

Media Contact

Anna Wood

Editor, International Trade Magazine

Tel: +44 (0) 1622 823 922

Email: editor@intrademagazine.com